Blockchain technology is coming to radicalize business as we know it.

Blockchain technology is often talked about in conjunction with cryptocurrency. This is only natural as the technology was developed in order to make cryptocurrency viable. However, blockchain technology is quickly being adapted into everyday business, in the same way that the cryptocurrency market is becoming just another market to invest in.

Today we’re going to look at how blockchain technology is projected to grow, its business impact, and how blockchain is entering into the cultural lexicon.

What Makes Blockchain Technology Work?

The three central tenets of blockchain technology are: 1) Decentralization, 2) Openness, and 3) Rigidity.

1) Decentralization. A lot of what we do in life requires a centralized service. Want to send a wire? It needs to go through a clearing firm. Recordkeeping, transactional data – it’s all kept on centralized databases that can be broken into, it requires updates, and can be corrupted. In addition, there are the maintenance costs.

Blockchain technology is not centralized. Information is not kept in one singular location but is spread out across an entire network. The only two entities involved in a transaction are those participating in it, dissolving the need for centralized authority.

2) Openness. As mentioned above, operations on the blockchain are open source. Anyone within the network can see it. However, the users’ identities are completely private via encryption, merely represented by a public address.

Transactions are recorded using a numerical code, a string of letters and numbers. This allows simultaneous openness and privacy. Without the encryption key, that string cannot be deciphered. This level of transparency creates greater accountability.

3) Rigidity. Once a new block on the chain has been created, it cannot be altered due to the technology’s cryptographic hash functions.

What Is Driving The Growth?

A recent projection estimates global blockchain technology market size to reach $64.09 billion by 2027. That’s a 56.1% compounded annual growth rate (CAGR) during the forecast period, up from $2.01 billion in 2019.1

Growth can be attributed to both the public and private sectors. The U.S. government has implemented blockchain program sectors such as defense & military, banks, and airports. While tech companies like Microsoft and Oracle would be natural fits for the development of new technology, non tech companies such as JP Morgan Chase and Deloitte, a bank and an accounting firm respectively, have also poured significant resources into blockchain.

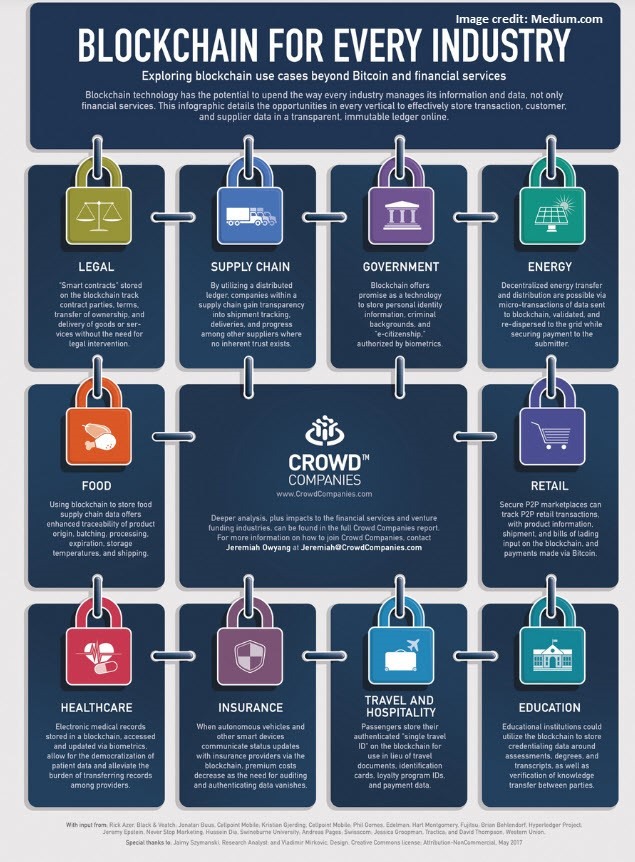

The below infographic from Banyan Hill2 is a fantastic, easy-to-read chart illustrating some of the major industries being impacted by blockchain:

Blockchain is still a new technology, a relative unknown. To most people, blockchain exists mainly in the world of cryptocurrency, a space far away from their everyday lives. They don’t understand it, so they fear it. They fear what kind of upheaval it will have on their businesses and their day-to-day lives. Until one day, if the projections are correct, the technology will become ubiquitous in daily life. It will become normalized. Normalization viewed through the lens of innovation could come off as a pejorative when it is the exact opposite. Normalcy leads to acceptance. Acceptance breeds change.

Hollywood Enters the Blockchain Game

Piggybacking off of the popularity of NFTs, Fox is in development on a new animated show, Krapopolis, that will become “the first-ever animated series curated entirely on the blockchain.”3 Beacon Pictures also announced in March that is developing a 10-part comedy series, Hold On For Dear Life, that will be financed using blockchain technology. It will also pay out crypto tokens to investors.4

Why does that matter?

While sitcoms may seem trivial in comparison to financial institutions and healthcare applications, what the masses consume can influence views on what is or is not normal.

In a 2016 Yale University study on normalcy, researchers posit that the idea of normality is neither entirely social nor statistical, but a combination of both. What is normal fluctuates. If something is presented to the public nonchalantly, eventually people almost subconsciously agree to accept that thing as normal.5 Entertainment can obviously impact this idea because it has a direct reach into the consumer.

With involvement by mass media, the concept of blockchain technology is now crossing over from obscure, techno-babble that must be sought out, into a product that can be seen. It takes something conceptual, a decentralized ledger, and turns it into something easily understandable – a television show. Not a cryptocurrency token, not a trust document, but something people can see and understand.

That, more than anything, might turn the radical into the mundane.

Joe Gallina

Joe has a degree in Finance from the University of Illinois at Chicago. Afterwards, he worked for Morgan Stanley and Bank of America/Merrill Lynch, obtaining both Series 7 and 66 licenses. At Merrill, he was on the self-directed side of the business, exposing himself to every aspect of the financial services industry.

Copyright © 2021 Protinus. All rights reserved.

1. https://www.globenewswire.com/en/news-release/2021/04/27/2217572/0/en/Blockchain-Market-to-Expand-at-56- 1-CAGR-and-Reach-USD-69-04-Billion-by-2027.html

2. https://banyanhill.com/top-trade-for-blockchain-boom-amplify-etf/

3. https://deadline.com/2021/05/dan-harmon-animated-series-krapopolis-blockchain-nfts-fox-1234758337/